2022 Q4 tax payments are due January 15. Automatically make your quarterly tax payment to the IRS through Catch.

One of the most thrilling things about striking out on your own is the freedom to structure your operations the way you see fit. You can work when you want, take the clients you want, and organize the way you want.

Yet, one of the scariest things is that there’s no structure in place for the not so fun parts of self-employment: taxes. When you don’t have an employer and HR department handling your tax withholdings, you may find yourself faced with conflicting or confusing information. That's actually the main reason we built Catch.

This guide can help you get started handling your taxes like a pro. And with Catch’s support for automatic tax withholding and payments, you could soon find yourself breezing through tax season with no significant anxiety attacks. Here’s how to do taxes as a freelancer (even if this is your first time!).

Step 1: Define Your Entity

The tax code is complex and based in large part on the type of business you have. Defining your entity is the first crucial step to untangling your tax requirements.

Employee vs. Independent Contractor

For some of you, the first step will be determining your classification. If you work in a place like a hair salon or you’re a writer for a company, you may not be clear on what your actual employment status is. Before you even worry about your taxes, consider this:

- Do you receive a W-2? You’re a full or part-time employee and don’t have to worry about your taxes for this position. Your employer has you covered.

- Do you receive a 1099-MISC? You’re an independent contractor with the company and will need to handle your own tax situation.

If you haven’t received a tax form yet, go ahead and ask your employer what your official designation is. If you feel you’ve been misclassified, you can read up on how to tell at our classification guide here.

Sole Proprietor

A sole proprietor is often the first step in venturing out on your own business. Sole proprietors report their expenses on a Schedule C report, and business profit and loss appears on the personal tax return.

Sole proprietorships don’t require you to file with the state to form and are easy to form and operate. However, you’ll be personally liable for what happens in the business. As you operate under this entity, you’ll need to fill out any or all of these forms to ensure you’ve handled your tax burden.

Partnership

If you aren’t the only owner of your business, but you aren’t ready to incorporate yet, you can operate under a Partnership. This entity doesn’t require state filing to set up and is taxed and managed similarly to a Sole Proprietorship.

Partners are personally liable for the business, and there’s no separation between business and personal assets. Owners also report their share of profit and loss through their personal income tax reports.

You may need to file different tax forms depending on your state and what you’re responsible for at the federal level.

Limited Liability Companies

If you’ve moved beyond sole proprietorship or couldn’t begin there, or your business has grown large enough that it makes you nervous to be personally liable for everything that happens, an LLC could be your next stop.

LLC designations have independent legal structures that are separate from their owners. An LLC separates your business and personal assets but is taxed similarly to a sole proprietorship (if you’re solo) or a partnership (if you’re not).

LLCs have different state regulations for who can be a member and what types of companies are eligible for an LLC. Federal law doesn’t designate one type of tax process for LLC entities either, giving owners the chance to choose a form of taxation that best suits the business. You can find out about potential forms here or more information about what constitutes an LLC here.

C Corporations

Now we’re getting into bigger, more complicated tax structures. If you have a C Corporation, you may have a finance person already handling the day to day accounting, but just in case, here’s what you need to know.

C Corporations are another way to separate your personal and business assets. They can have multiple owners and are taxed on shareholder dividends and corporate profits. Also, heads up, you’re going to have to hold those dreaded meetings.

C Corporations potentially are the employer filing on behalf of employees, so you’ll need your own W2 or 1099-MISC forms in addition to tax filing forms required on the federal and state level.

S Corporations

S Corporations are very similar to C Corporations but with more significant limitations on membership. S Corporations separate your business and personal assets, and liabilities and owners report their share of profit and loss on a personal tax return.

S Corporations also have to hold meetings, and state regulations limit who and how a business can incorporate under this entity. You may need to fill out multiple tax forms depending on your structure and liabilities.

Step 2: Figure Out Your Payments

There’s a lot of conflicting information out there about how to pay for your self-employment taxes. Do you file quarterly? Only at the end of the year? If you don’t have an accountant handling things for you, it’s easy just to stop paying.

If you’re a contract employee on the side but a full-time employee overall and don’t plan to make more than the threshold ($400) to file self-employment taxes officially, you can file at the end of the year with your personal income tax form. You may want to ask your employer to withhold a little extra from your full-time checks to help ensure your tax responsibilities are covered just to be safe.

If self-employment is your gig, the IRS requires (in most cases) that you handle your tax responsibility through quarterly payments. These payments are due (though sometimes adjusted for the weekend):

- April 15

- June 15

- September 15

- January 15

If you expect to owe more than $1000 at the end of the tax year, you’ll want to make those quarterly payments on time, or the IRS may assess penalties and late fees even if you pay up at the end of the year.

The magic lies in estimating how much money you’ll make throughout the year and assessing your tax responsibility based on that estimate. If this is your very first year in business, that could seem impossible. Here’s a quick tip for making a logical estimation if you’ve never been in business before.

- Take a look at your fixed monthly expenses. You made the jump to full-time self-employment because you were pretty confident you could cover those. That number is your baseline estimate.

- Add on fluctuating extras like food, gas, entertainment, and anything else that’s subject to change. Add that number to your estimate.

- Take a good long look at how much you made when you were dabbling in your side hustle and decide if you can expand that number to a full-time approximation. Blend those numbers, and you’ve got a good estimate for how much you’ll make.

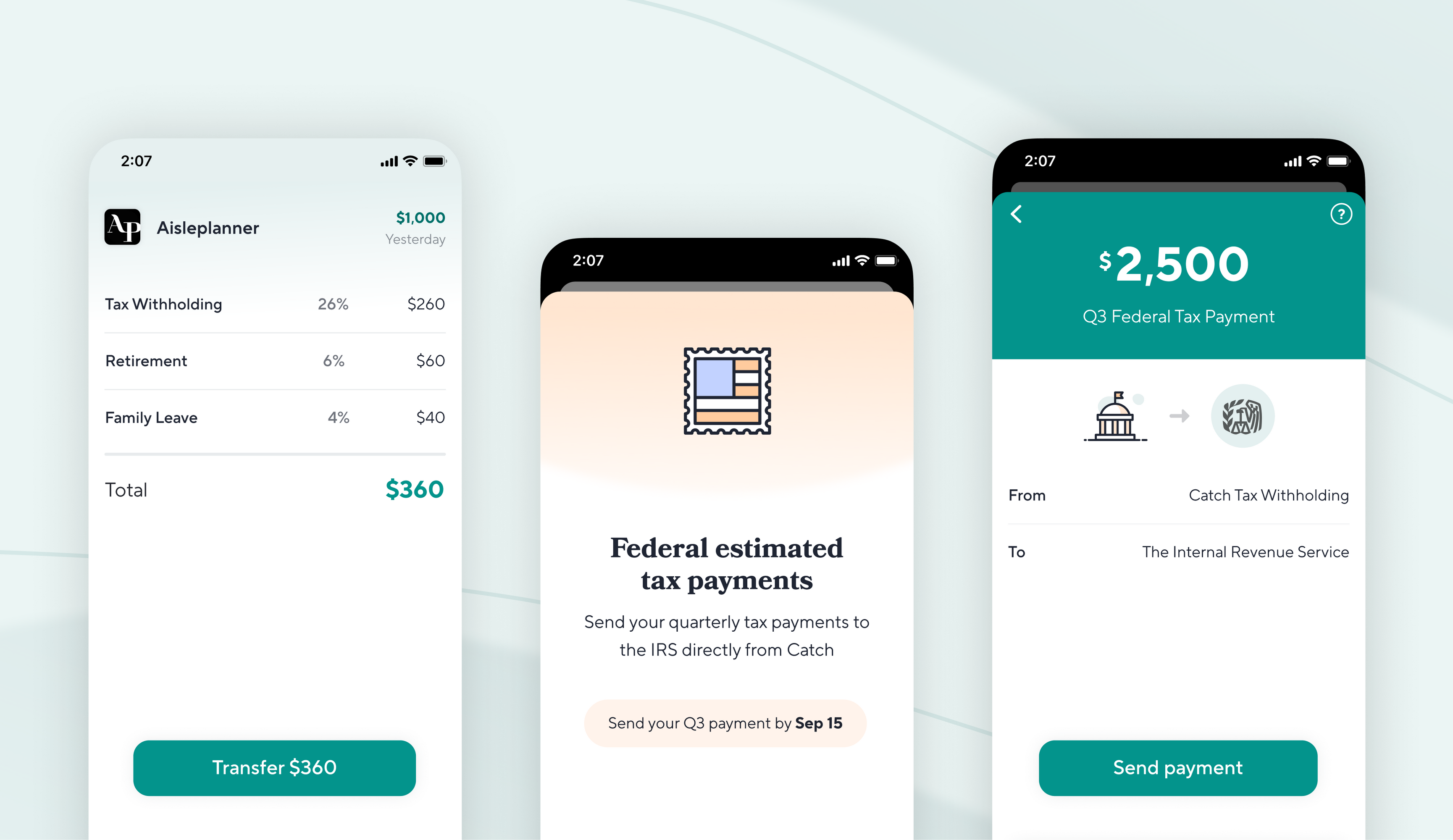

- Then, set up your Catch account to withdraw a percentage of each and every payment you receive, submitting the amount in full for each quarterly tax deadline. Catch recommends a percentage of each payment be withdrawn for taxes based on your state and federal tax bracket.

Catch helps you set aside part of each paycheck to stay on track.

Step 3: Calculate Your Deductions

And now the fun part. Deductions can help make the pain of taxes a little lighter. Business deductions can reduce your overall tax burden by accounting for things you use to help your business remain successful. Common tax deductions include:

- upfront costs for starting up (that computer you bought for your writing career, for example)

- ongoing costs (software that enables you to invoice)

- business memberships

- continuing education

- mileage

- home office or office rental

- office supplies

- fees (like Paypal’s business fees)

You may want to research your particular field of work to find specific deductions. Hairdressers may be able to deduct furniture, for example, or photographers may deduct their flash equipment.

If you aren’t sure what deductions to take, you may want to discuss more complex deductions with a proper financial authority who can answer questions about appropriate deductions so that you don’t have to pay penalties later.

Step 4: Set Up Your Tax Forms

Here’s what you need to know about filing quarterly taxes and your annual return.

How to File My Quarterly Taxes

- The easiest thing to do is pay your quarterly taxes directly through Catch. Each quarter, just tell us how much to send from your withholding, and we'll take care of the rest.

OR you can do it yourself.

- You’ll need to set up an account with the IRS to pay your quarterly taxes. You’ll need your social security number or your EIN (if you’ve set one up). Set up an account to get started.

- Once you’ve got your account, use the IRS form 1040-ES to calculate your estimated tax responsibility. Divide by four to get your estimated quarterly tax payments.

- Pay your quarterly taxes by the due date (see above). Don’t worry if you make more or less throughout the year than what you were planning. You can adjust payments to account for a bigger or smaller profit.

- You can also use software like Quickbooks to track your income and deductions and estimate quarterly taxes based on your income.

- When you file your annual return, you’ll catch up on any further money owed by following through with your annual return much the way you did when you were a full-time employee.

How to File My Annual Taxes as a Freelancer

- You’ll need your 1099s from clients you’ve worked with for contract work. Note: Even if you do not receive a 1099, you are still liable for reporting any income you received for the tax year.

- If you have receipts to claim deductions, be sure you have those accounted for.

- Fill out the tax form or use tax software to calculate your tax responsibilities and any deductions you may use to reduce your tax burden.

- File your federal (and state and city if applicable).

- If you owe money, make arrangements as soon as possible to pay the taxes and any penalties. If the government owes you money, you can request it paid to you, apply it to previous tax burdens, or apply it to future payments.

Frequently Asked Questions:

- Do I have to file taxes? - If you’re a W2 employee, you will probably need to file. If you make more than $400 from your side hustle during the tax year, then yes, you’ll have to file self-employment taxes. If this is your side hustle, you may be able to add your 1099 to your personal return along with your W2, but either way, you’ll have to declare that income.

- Do I have to pay quarterly taxes? - If you suspect that you’ll owe more than $1000 in tax, you’re required to pay quarterly estimated taxes. If you aren’t sure you’ll owe that much, it’s still a good idea to make a quarterly payment just in case. If you don’t pay quarterly taxes and it turns out that you owe taxes at your annual return, the IRS may apply penalties and late fees, even if you pay what you owe right then. You can always get money back on your return if you way overestimate, so it’s better to be safe and make those payments.

- What happens if I owe a lot of money? - It can be scary to file taxes and wonder if you’ll owe a significant amount on your taxes at the end of the year. Instead of avoiding paying your taxes, you can set up payment plans with the IRS to handle your tax burden.

- What if I don’t pay? - The IRS can step in and take that money in many different ways, including garnishing your wages and taking any subsequent refunds. They may also pursue litigation. It’s best to pay. If you skipped a year filing taxes, the best thing to do is talk to a tax professional for advice on getting current as soon as possible. This is not something you want to avoid.

- How do I set up an account? - The IRS makes it simple to pay your estimated taxes. You’ll need your social security number or your EIN to identify you.

- Do I need an EIN? - Your social security number works fine, but reducing other people’s access to that number is an excellent reason to go ahead and apply for an EIN. It’s simple and instantaneous.

Getting Started with Your Self Employment Taxes

There’s a lot of software out there for putting together your taxes so you don’t need a CPA level knowledge for how to do taxes as a contractor. Catch is designed to pull money from your account only when you get paid, ensuring that you withhold the right amount and have money set aside for each quarter.

Getting your taxes started is a lot more intimidating than it has to be. For most freelancers, the entity is pretty straightforward, so taxes aren’t quite as complicated as you think. Even if you don’t get it exactly right, the IRS makes space for you to pivot and adjust before it’s a huge deal.

The worst thing you can do is ignore your tax burden because you’re too intimidated to get started. However, if you dive in and do your research, you’ll be able to get your taxes covered in no time.

Sign up with Catch to get started managing your taxes. It’s simple, automatic, and ensures you’re never left scrambling.